Energy efficient homes keep money in owners’ pockets

Energy efficient homes keep money in owners’ pockets

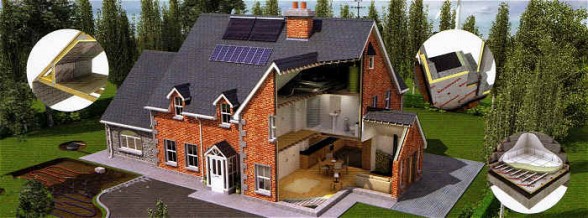

A study released March 19 and called “Home Energy Efficiency and Mortgage Risks” by the University of North Carolina at Chapel Hill suggests that if you own an energy efficiency home, you are a third less likely to default on your mortgage. The report provides strong evidence that homeowners are taking savings from efficiency and paying their mortgages on time. This raises again the issue of the potential for energy-efficient mortgages, where lenders give credit for efficiency upgrades that may be more important than credit scores in issuing loans.

The study used a sample of 71,000 home loans from across the country originated between 2002 and 2012. Researchers found that mortgages on homes with Energy Star certifications were 32% less likely to default than were loans on homes with no energy-efficiency improvements. (Energy Star certified homes are up to 30% more efficient than code.)

Researchers statistically isolated factors that might account for the different performances by borrowers on their mortgages. They controlled for house size; age of the house; neighborhood income levels; house values relative to the area median; local unemployment rates; borrowers’ credit scores; loan-to-value ratios; electricity costs; and even local weather conditions. The average sale price of both the energy-efficient homes and the others was $220,000, removing the possibility that the energy-efficient properties were high-end houses purchased by families less likely to default.

Washington Post contributor Ken Harney points out that there’s the problem with the way the mortgage system treats energy efficiency: “Under current practices, you’d be hard-pressed to find any lenders who’ll give you a better rate quote on your mortgage application, even if you showed them your Energy Star certification along with documentation that your house saves buckets of money on utility bills.” These are factors that lenders and Congress should consider when making mortgage policy.

Concurrent to the release of the University of North Carolina study, the 9th Circuit Court of Appeals has vacated the district courts order and dismissed the lawsuit against the FHFA regarding PACE financing. The court ruled that the FHFA acted in its role as conservator of Freddie Mac and Fannie Mae, and thus that the courts have no jurisdiction. Similar rulings in favor of FHFA were rendered in New York and Florida, in the second and eleventh circuits. At this time, and despite over 40,000 comments, the FHFA may abandon its rulemaking process ordered by the District Court for the Northern District of California.

PACE has been seen as a game-changer for energy efficiency, especially for those with limited access to capital for efficiency upgrades and renewable energy systems. Now Freddie Mac and Fannie Mae will not purchase mortgages with superior liens, and the result will be regressive. Those that qualify for (and need) conforming loans will not be able to enjoy the benefits of energy efficiency and renewable energy system upgrades enabled through PACE that will leverage greater and greater savings over time. The ruling denies smart investments.

The 20 latest Blog Posts

- Flanigan’s Eco-Logic Podcast featured in Feedspot’s Top 15 California Sustainability Podcasts

- Vol.26 #3: Diet, Happiness, Dancing

- Vol.26 #2: Solar is Surging

- EnerTech Partnership Announcement

- Vol.26 #1: The Times They Are a’Changing

- Join Us As We Bring in the New Year!

- Vol.25 #12: Electric Vehicle Charging

- Vol.25 #11: The Climate Reality

- Vol.25 #10: Bloated Cars

- Vol.25 #9: The End of Range Anxiety

- Vol.25 #8: Father of the Bride

- Vol.25 #7: Electric Vehicle Charging Networks

- A Review of Operations and Maintenance Providers for Aging Solar Solar Systems

- Vol.25 #6: The Renewable Tipping Point

- Residential Solar-Ports: A Pictorial Review of Household Options

- Vol.25 #5: Crafting Intentional Community

- Vol.25 #4: Celebrating Rocky Mountain Institute’s Impact!

- Vol.25 #3: Oyster Bay

- Vol.25 #2: The EV Revolution

- Vol.25 #1: Untapped Solar Potential, Sustainable Aviation, and Cigarette Butt Accountability

Available Pages

- #7101 (no title)

- “Microgrid Knowledge” Features EcoMotion in an Article Highlighting Lessons Learned in Microgrid Development

- “Reggie” Doubles Down in New England

- 2013 New England SAVE A TON Campus Tour

- 2013 New England SAVE A TON Tour visits Brown, Yale, Clark, and More

- 23 Megawatts of Solar

- 2nd Annual Energy Innovation Tour is December 7th

- 2nd Annual Energy Innovation Tour Picture Gallery

- 48-Campus Solar Feasibility Assessment

- A Brief Investigation into Battery Degradation During Normal Cycling Conditions and Standby Operations

- A Review of Operations and Maintenance Providers for Aging Solar Solar Systems

- Accomplishments

- Accomplishments

- Accomplishments

- Accomplishments

- ADDITIONAL CITY SERVICES

- Affordable Economics

- Agrivoltaics and Shared Light

- Alaska Housing Finance Corporation, Alaska Craftsman Home Program

- Alberta Power, Jasper Energy Efficiency Project

- Alizeh Siddiqui Joins EcoMotion as Project Manager

- Almond Farming and California Water

- Americans Believe in Climate Change

- An Overview of the EV Market

- Ancillary Services from Distributed Storage

- Andrew Waddell Joins the EcoMotion Team as Solar Project Manager

- Background on Community Choice Aggregation

- Battery Back-up, Solar, and Prop 39 Santa Rita Unified School District – Salinas, California

- Best Practices at the Greenest Airports

- Biofuels: The Second Generation

- Blockchain White Paper

- Bonneville Power Administration, Energy $avings Plan

- Bonneville Power Administration, Energy Smart Design

- Bonneville Power Administration, Hood River Conservation Project

- Bonneville Power Administration, Manufactured Housing Acquisition Program

- Bonneville Power Administration, Super Good Cents

- Bonneville Power Administration, WaterWise

- Boston Edison, Large C/I Program

- Boston Edison, Large C/I Program

- Boston Edison, Residential Efficient Lighting Program

- Boys and Girls Club of Pomona Valley Celebrates Earth Day with New Solar System

- British Columbia Hydro, Power Smart High-Efficiency Motors Program

- British Columbia Hydro, Power Smart Refrigerator Buy-Back Pilot

- British Columbia Hydro, Process Improvements Program

- Bryant University’s June Candland Joins EcoMotion as Intern in Rhode Island

- Buckeye Power, Residential Load Control

- Building Codes and the Westside Urban Forum

- Burbank, Anaheim Contract with EcoMotion for Solar Validation Services

- Burlington Electric Department, Comprehensive DSM

- Burlington Electric Department, Heat Exchange

- Burlington Electric Department, Smartlight

- Buying Clean Air in a Can

- California Energy Commission, Energy Partnership Program

- CALIFORNIA PROP 39 SERVICES

- California’s Cap and Trade Extended

- California’s Cap and Trade Starts

- Campus Services Providing STARS Assessment for Central New Mexico Community College

- Campuses

- Capital Group Companies Amplifies Solar in Irvine

- Central Maine Power, Operation Lightswitch

- Changes as Solar Santa Monica Heads Into Third Year with EcoMotion

- China’s energy Director Chen Hosted by EcoMotion

- Chipping Away at My Footprint

- Cities

- Cities Heading to 100% Renewable Power

- City of Ashland, Comprehensive Conservation Programs

- City of Austin Energy Services Division, Comprehensive DSM

- City of Austin, Texas, Energy Star Rating

- City of Austin,TX, Green Builder

- City of Beverly Hills Hires EcoMotion to Develop Solar Strategy for Municipal Facilities

- City of Palo Alto, Point of Purchase Pilot CFL Program

- City of Phoenix, Energy Management/Capital Reinvestment Plan

- Clarifying RECs and Carbon Offsets

- Clean Energy Jobs Dwarf Dirty Ones

- CLIMATE AND ENERGY ACTION PLANS

- Coachella Valley Takes Next Step in Regional Energy Planning with EcoMotion’s Help

- Codi Leitner Joins the EcoMotion Team as Assistant Project Manager for Business Development

- Community Solar Plants

- Community Solar: Design Options and Innovations

- Commuter CFL Giveaway

- Congestion Pricing and Flying Taxis

- Consultant Team

- Contact

- COP23 – a Salute!

- Copenhagen, Denmark, Comprehensive Municipal Energy Efficiency

- Cornwall, Ontario , Energy Efficiency Team

- Corporations

- Creating and Financing Six, Carbon-Free Microgrids for Santa Rita Union School District

- Creating Microgrids and PERCs: Powered Emergency Response Centers

- Cusco and the Sacred Valley

- Cyber Attacks and Connected Vehicles

- Data Centers as the New Smelters

- Digging the Green Schools Movement!

- Divesting Fossil Fuels and Prisons

- Driving smart

- Duct Testing and Repair Programs

- Duquesne Light Company, Smart Comfort

- Eco-Towns

- EcoGroup, In Concert With The Environment

- EcoMotion and AASHE Partner on Campus

- EcoMotion and Climate Resolve Launch “Climate Smart Schools”

- EcoMotion and the SBCCOG to Guide Eight South Bay Cities to SolSmart Designation

- EcoMotion Brings Sun Power to Anaheim Schools

- EcoMotion Brings Sun Power to Anaheim Schools

- EcoMotion Co-Hosts Third Annual 2015 Sustainability UnConference in Boston on Earth Day, April 22

- EcoMotion Completes Alignment Solar Feasibility Analysis for Metro

- EcoMotion Completes Corporate Sustainability Plan for Roy Jordensen Associates, Inc.

- EcoMotion Conducts ASHRAE Level I Audit of Shopping Center on St. Croix

- EcoMotion Conducts PV Operations and Maintenance Training for LA Metro

- EcoMotion Continues for Fourth Year as Program Consultants to Solar Santa Monica

- EcoMotion Conversations with Jigar Shah

- EcoMotion Coordinates 2nd Annual Sustainability unConference at District Hall in Boston

- EcoMotion Debutes Solar Santa Monica on National Stage

- EcoMotion Delivers Solar 101 Webinar for the Association of College and University Housing Officers

- EcoMotion Facilitates Monthly Massachusetts Sustainability Coordinators Roundtable

- EcoMotion Facilitates STARS Workshop in New Mexico

- EcoMotion Guides Millbrook School To Being 100% Solar-Powered with 1.73 MW Solar Field Powered by SolarCIty

- EcoMotion Helps Bryant Achieve STARS Silver in Rhode Island

- EcoMotion Helps Central New Mexico Community College to Achieve STARS Bronze Sustainability Rating

- EcoMotion Holds Energy Financing Seminar

- EcoMotion Hosts Korean Delegation on Zero Energy Fact Finding Mission

- EcoMotion Hosts Solar Expert

- EcoMotion Is Advisor to Capital Group Companies for Largest Solar Installation in Orange County

- EcoMotion is Certified by the City of Los Angeles Green Business Program

- EcoMotion is Hiring! Campus Sustainability Coordinator to Serve New England Clients

- EcoMotion Joins University of Phoenix in Solar System Donation

- EcoMotion Leads 2009 Solar Research Tour to Spain

- EcoMotion Leads 2009 Solar Research Tour to Spain

- EcoMotion Moves into Historic Offices at One Bunker Hill, 601 Fifth Street, Los Angeles

- EcoMotion Named West Hollywood’s Solar Adviser

- EcoMotion Participates in “Living Pilot” Symposium in San Francisco

- EcoMotion Releases RFP for 1.6 MW Solar System in New York

- EcoMotion Releases White Paper on Fossil Fuels Divestment Campaigns

- EcoMotion Represents California at Asia Clean Energy Forum

- EcoMotion Retained by Thayer Academy for Sustainability Coordination and Three Initial Services

- EcoMotion Selected by East Bay Community Energy

- EcoMotion Selected by Santa Monica to Promote Energy Upgrade California

- EcoMotion Serves as Owner’s Rep for Cathay Bank Solar Project

- EcoMotion Solar Uncovers $251,000 Annual Bill Error for Santa Monica

- EcoMotion Takes “Best Green Know-How” to Korea

- EcoMotion Takes “Best Green Know-How” to Korea

- EcoMotion to Assist Brea in City-wide Efficiency Planning

- EcoMotion to Promote Solar on North American Campuses with AASHE

- Ecomotion Trains LA Metro on Preventative Maintenance for Solar Systems

- EcoMotion Welcomes Barry Murrey, our New Business Development Manager

- EcoMotion Welcomes Interns in Rhode Island and Massachusetts

- EcoMotion Welcomes New Intern in Southern California, Ben Meissner

- EcoMotion Welcomes Spring Semester Intern, Sasha Srivastava

- EcoMotion Welcomes Spring Semester Intern, Stefano Fantuzzi

- EcoMotion Welcomes Talia Arnow to the Campus Services Team in Cambridge, Massachusetts

- EcoMotion Works to Save the World

- EcoMotion Works: Energy Storage in Irvine, CA

- EcoMotion’s Progress Quantifying Campus Sustainability

- EcoMotion’s Solar Contractor Database

- EcoMotion’s Sustainability Accelerator Toolkit

- EcoMotion’s Sustainability Tips

- EcoMotion’s Ted Flanigan Harvests 37 Energy Saving Ideas at High Sierra Fest

- EcoMotion’s Ted Flanigan Presents Carbon-Free Energy Resilience at Venture Café Global Earth Night Webinar

- EcoMotion, the Hub, and CIC host first Cambridge Sustainability unConference

- EcoMotion’s Energy Efficiency Works

- EcoMotion’s Top 10 2020 Highlights

- EcoNet News

- EcoNet News Vol. 21 #2: The Milkman Model & Air Quality in Schools

- EcoStream

- EcoStream Case Study: Adams 12 Five Star Schools

- EcoStream Case Study: Concord Academy’s Sustainability Plan

- EcoStream Case Study: Fairfax County Public Schools Greenhouse Gas Inventories

- EcoStream Case Study: Food and Conservation Science at Hood River Middle School

- EcoStream Case Study: Glendale Community College Energy Strategy Validation Study

- EcoStream Case Study: Hanover High School

- EcoStream Case Study: Oak Park Unified School District

- EcoStream Case Study: Phillips Andover Academy 2019-2030 Climate Action Plan

- EcoStream Case Study: San Francisco Unified School District (SFUSD)

- EcoTip

- EcoTip

- EcoTip

- El Nino Southern Oscillation

- Electric Buses in Focus

- Electricite de France, Operation: LBC

- Emily Schweitzer

- Emily Schweitzer Joins EcoMotion Campus Services in New England

- Energy Efficiency and Demand Response Programs Savings

- Energy Efficiency Message Scores at Orange County Helios Awards

- ENERGY EFFICIENCY SERVICES

- Energy in Obama’s First Term

- Energy Rated Homes of America, Uniform Energy Rating System

- Energy Resilience and Microgrids

- Energy Resilience Podcast

- Energy Resiliency in Santa Monica

- Energy Services Agreements

- Energy Storage in Focus at Green Energy Entrepreneur Series Workshop #2 at UC Riverside April 21st

- Energy Storage White Paper: “The Lithium-Ion, Hybrid Building Revolution”

- Energy, Mines and Resources Canada, R-2000

- EnerTech Partnership Announcement

- Environmental Apps for Sustainability

- Environmental Protection Agency, Green Lights

- Environmental Resource Center, Destination Conservation

- EUA Cogenex, U.S. Department of Energy’s Forrestal Building Retrofit

- Exterior Lighting Project in Murrieta

- First Commercial Electric Aviation

- First Florida City Signs Solar Ordinance

- First of Ten Anaheim Elementary Schools Gets its “Solar Flag”

- Fisher College Signs with EcoMotion for Campus Greening Services

- Flanigan’s Eco-Logic Podcast

- Flanigan’s Eco-Logic Podcast featured in Feedspot’s Top 15 California Sustainability Podcasts

- Flanigan’s Eco-Logic: No-Cost Carbon Neutrality

- Flanigan’s EcoLogic: Big and Bold Green Steps!

- Flanigan’s EcoLogic: Hitting Recycling Hard

- Florida Power Corporation, Residential Load Management

- Flow Batteries for Cars

- Ford and Toyota Lead Plug-in EV Sales

- German Solar Program

- GGUSD Wins $2 Million Grant from Water Resources Control Board thanks to Climate Smart Schools

- Glendale Hires EcoMotion to Establish Sustainability Office

- Golden State Policy Advances

- Goldman Sachs to Invest $150 Billion in Clean Tech

- Green Energy Entrepreneur Series Features Solar Experts from PermaCity, SolarCity and Brightsource

- GREENHOUSE GAS INVENTORIES

- Grid Reliability

- Hannover, Germany, Comprehensive Municipal Energy Efficiency

- Home

- Homes a Third Less Likely to Default

- Hubway Bike Sharing

- Hydrogen – The Invisible Fire

- IEA Reports Dramatic Rise of Renewables

- Introducing Jibade Sandiford, EcoMotion’s Newest Solar Project Manager

- Iowa Department of Natural Resources, Energy Bank Program

- Jay Baldwin Joins EcoMotion as Business Development Director

- Jessica Wolfert

- Join Us As We Bring in the New Year!

- Jonathan Parfrey

- Jonathan Port

- June 20, 2018, Accelerated Energy Investment Forum

- Lancaster Mandates Solar

- LA’s 141,089 Unit LED Street Lighting Success

- Leicester, England, Comprehensive Municipal Energy Efficiency

- Lima

- Local Government Sustainable Energy Coalition Microgrid Webinar

- Luskin’s 100% Clean Energy Summit – Ted Flanigan Reports

- Machu Picchu Travelogue: Trekking Peru Days 3 & 4

- Madison Gas and Electric, Residential Lighting Program

- Mass DOT Goes Solar

- Media

- Meet Our New Staff Engineer Brady Zaitoon P E LEED AP

- Metro Solar Preventative Maintenance Tutorials

- MICHAEL WARE

- Microgrids 101

- Microgrids and Smart Grids in Focus at Green Energy Entrepreneur Workshop in San Bernardino

- Midwest Resources, Rock Valley Energy Efficiency Research Project

- Millbrook School on the Path to Carbon Neutrality… 100% Solar Powered

- Millbrook School Selects EcoMotion as Solar Advisor

- Minneapolis Center for Energy and Environment, Multi-family retrofits

- Montgomery County Maryland, Resource Conservation Program

- Montgomery County Maryland, Resource Conservation Program

- Moreno Valley Utility (MVU) Announces 2008 Solar Special

- Moreno Valley Utility (MVU) Announces 2008 Solar Special

- Never-Charge Electric Vehicles

- New and Old Geothermal

- New England 2013 SAVE A TON Tour Wraps Up at Yale University

- New England Electric System, Residential Electric Space Heat

- New Podcast with Michael Ware

- New Podcast: A Conversation with Michael Peevey and Diane Wittenberg

- New Summer Internship Opportunity

- New York Power Authority, High Efficiency Lighting Program

- Niagara Mohawk Power Corp., Subscriptive Service

- Niagara Mohawk Power Corp., Subscriptive Service

- Nicols Wins Bronze TELLY with Energy Video

- Northeast Utilities, Lighting Catalog Program

- Ontario Hydro, Espanola

- Osage (Iowa) Municipal Utility, Comprehensive DSM Program

- Oslo, Norway, Comprehensive Municipal Energy Efficiency

- Otter Tail Power Company, House Therapy and Appliance Aid

- Our Staff

- Overcoming Range Anxiety

- PACE Solutions: Bringing AB 811 Home

- Pacific Gas & Electric, Commercial New Construction

- Pacific Gas & Electric, Direct Assistance

- Pacific Gas & Electric, Model Energy Communities Program

- Pacific Gas & Electric, Showerhead Program

- Pacific Gas and Electric, PG&E Energy Center

- PacifiCorp, Large Commercial Energy FinAnswer

- Palm Desert AB 811 Conference, June 12, 2009, hosted by EcoMotion

- Palm Desert Council Approves Environmental Sustainability Plan and Greenhouse Gas Inventory

- Palm Desert Names Ted Flanigan as Senior Energy Policy Advisor

- Palm Desert Names Ted Flanigan as Senior Energy Policy Advisor

- Participating in the Milken Institute’s Summit California in Santa Monica

- Partnering with Sustainable Endowments Institute to Promote Green Revolving Funds in New England

- Peru at a Glance

- Philosophy

- Portland Energy Office, Multi-family Energy Savings Program

- Portland General Electric, Energy Smarts for Schools

- Powered Emergency Response Centers (PERCs) at Santa Rita Union School District

- Powered Emergency Response Centers (PERCs) Updates

- Preferred Resources and 100% RPS Aspirations

- Production and Investment Tax Credits

- Prop 39: The Santa Rosa Story

- PSI Energy, Smart $aver Homes

- Public Service of Oklahoma, Ground Source Heat Pump Research Project

- Ralph Torrie

- REGIONAL ENGAGEMENT

- Renewable Energy Leadership

- Renewable Energy Master Planning for Loyola Marymount

- Renewables at 12% and Rising

- Renewables Outpace Nuclear

- Residential Solar-Ports: A Pictorial Review of Household Options

- Results Center – Test

- Rick Heede

- Saarbrücken, Germany, Comprehensive Municipal Energy Efficiency

- Sacramento Municipal Utility District, Commercial Lighting Installation Program

- Sacramento Municipal Utility District, Comprehensive DSM

- Sacramento Municipal Utility District, Residential Peak Corps

- Sacramento Municipal Utility District, Solar Domestic Water Heating

- Sample Page

- Sample Page

- San Diego Gas and Electric, Commercial Lighting Retrofit

- Santa Monica Project Awarded to EcoMotion

- Save a Ton Campaign

- School District of Philadelphia, Save Energy Campaign

- Seattle City Light, Comprehensive Municipal DSM

- Seattle City Light, Lighting Design Lab

- Seattle City Light, Low Income Electric Program

- Second Demonstration “Solar Flag” Goes Up in Anaheim

- Services for Cities

- SIERRA FLANIGAN

- SIGNATURE CAMPUS SUSTAINABILITY APPROACH

- Snow and Ice Melt Systems: Frequently Asked Questions

- Solar

- Solar Co-ops Community Power Network Style!

- Solar Expert Troy Strand Welcomed into EcoMotion’s Consulting Stable

- Solar Industry Employs 173,807 Americans

- Solar Plus Energy Storage Microgrid Kickoff Event

- Solar Power in the Middle East

- Solar Powers up the Emissions Time Bomb for Earth Day at UCR!

- Solar Santa Monica Kicks Off

- Solar Santa Monica Recognized by U. S. Conference of Mayors for Climate Protection

- SOLAR SERVICES

- SOLAR SERVICES FOR CITIES

- SOLAR SERVICES FOR YOUR CAMPUS

- Solar Workshop in Carson!

- Sonoma County Asks EcoMotion to Assist with Feasibility Study for AB 811 Program

- Sonoma County Asks EcoMotion to Assist with Feasibility Study for AB 811 Program

- Southern California Edison, CFB Manufacturer’s Rebate

- Southern California Edison, CFB Manufacturer’s Rebate

- Southern California Edison, Low Income Relamping

- Southern California Energy Summit

- Southwestern Electric Cooperative, Inc., Geo-Lease

- Speaking

- Stanford Reaches for the STARS…

- State of Texas, LoanSTAR Program

- State University of New York at Buffalo, Comprehensive Energy & Resource Mgmnt

- Sumin Sohn Joins the EcoMotion Team as Prop 39 Project Manager

- SUSTAINABILITY PLANNING

- Tacoma Public Utilities, Fort Lewis Electric Efficiency Retrofit

- Talia Arnow

- Taxis

- TED FLANIGAN

- Ted Flanigan Gives Keynote Address at CleanTech Law Summit

- Ted Flanigan Guest Lectures at Harvard Law School

- Ted Flanigan Interviews Jigar Shah of Generate Capital for New Podcast

- Ted Flanigan Interviews Senator Henry Stern for YPE

- Ted Flanigan Leads Session on Effective Program Messaging at 26th E Source Forum in Denver, Colorado

- Ted Flanigan Speaks at 5th Annual E Source Conference

- Ted Flanigan Speaks at DeCarbonizing California: 2020 – 2050, Hosted by Climate Resolve

- Ted Flanigan Speaks at LAUSD School’s Career Day

- Ted Flanigan Speaks for Garden Grove Unified at CASBO 2015 Annual Conference in San Diego

- Ted Flanigan Speaks on Solar PPAs at SEC Forums in Sacramento, Riverside, and Santa Ana

- Ted Flanigan to Speak about Microgrids at Impact Investing Forum

- Ted Flanigan’s Trinity Broadcasting Network “Carbon Footprint Interview” Now on YouTube

- Ted Flanigan’s Trinity Broadcasting Network “Carbon Footprint Interview” Now on YouTube

- Ted Speaks at the School Energy Coalition Spring Summit

- The 31-State Climate Registry

- The Amazon

- The Benefactor Investment Model: a new way to finance clean energy projects

- The Dawn of Vertical Forests

- The Federal Clean Power Plan

- The Food Truck Fling Energy and Carbon in Focus

- The Fortune 500 Nears the Tipping Point

- The Green Corps

- The Hawaiian Power Update

- The Inca Trail

- The MPG of Electric Vehicles

- The Next Secretary of Energy’s Agenda

- The Philippines, Residential AirCon Standards and Labeling

- The Power Sector

- The Reality of Negative Emissions

- The Results Center

- The Rise of Prosumers

- The San Onofre Challenge

- The Solar Santa Monica Feed-In Tariff White Paper

- The State of Solar on Campus 2014 Edition

- The Tiny House Movement

- The U.C. San Diego Microgrid

- The Wireless Future of Energy

- The World Heritage Archeological Site

- Thelma Rodriguez-Winter Joins EcoMotion’s Climate Smart Schools Team

- There’s Energy Resilience in the Garage! An Essay on Electric Vehicles and Emergency Back-Up Power

- Three Trillion Trees

- Todd Flora joins EcoMotion as Director of Business Development in California

- Tony Pierce

- Touring the Salton Sea Region

- Transit Buses: The Advent of Electrification

- U.S. on Target to Meet Climate Commitment

- unConference Draws 300 Earth Day Participants Boston’s District Hall

- United Illuminating, Energy Blueprint

- United Illuminating, Homeworks

- United Power Association, Off-Peak Program

- United States Rejoins the Paris Agreement

- University of Southern California Hires EcoMotion for Galen Center Solar

- Unpacking Energy Resilience: From Generators to Carbon-Free Microgrids

- UTILITY PROGRAMS

- UTILITY SERVICES

- Videos

- Viewers to Volunteers: Support Causes for Free with this App

- Visiting LA Department of Water and Power’s Pine Tree Wind and Solar Farm

- Visiting the Cuttyhunk Microgrid

- Vol. 10 #1 – March 2006: Introducing the EcoMotion Network

- Vol. 10 #10, August 17, 2006: Lifestyle Edition

- Vol. 10 #11, August 31, 2006: Hybridization

- Vol. 10 #12, September 19, 2006: Urban Water Trade-Offs

- Vol. 10 #13, October 4, 2006: Energy Financing

- Vol. 10 #14, October 25, 2006: Global Changes

- Vol. 10 #15, November 10, 2006: Bio-Cycling

- Vol. 10 #16, December 6, 2006: The Household Edition

- Vol. 10 #17, December 29, 2006: CFL Issue

- Vol. 10 #18, January 12, 2007: Happy New Year!

- Vol. 10 #19, January 26, 2007: Solar Santa Monica

- Vol. 10 #2, March 29, 2006: Taking Action

- Vol. 10 #20, February 16, 2007: Clean Air

- Vol. 10 #21, March 1, 2007: Mayors for Climate Protection

- Vol. 10 #22, March 16, 2007: Tipping Point

- Vol. 10 #23, April 6, 2007: Solar Update

- Vol. 10 #24, April,18, 2007: Worldwide Action

- Vol. 10 #25, May 4, 2007: Generation Shift

- Vol. 10 #3, April 14, 2006: Denmark and Iceland

- Vol. 10 #4, April 28, 2006: China’s Water Crisis

- Vol. 10 #5, May 15, 2006: Naked Truths

- Vol. 10 #6, May 26, 2006: Fuel Cell Trains

- Vol. 10 #7, June 14, 2006: An Inconvenient Truth

- Vol. 10 #8, July 14, 2006: Mammoth’s List of 37

- Vol. 10 #9, July 28, 2006: Heat Wave

- Vol. 11 #1, May 21, 2007: Climate News

- Vol. 11 #10, November 27, 2007: Policy Actions

- Vol. 11 #11, December 11, 2007: The California Feed-In Tarriff

- Vol. 11 #12, January 9, 2008: Healthy or Poison?

- Vol. 11 #13, February 15, 2008: Momentum

- Vol. 11 #14, March 19, 2008: Long Beach Special

- Vol. 11 #15, April 10, 2008: Miami City Hall

- Vol. 11 #16, April 25, 2008: Horsepower

- Vol. 11 #17, May 9, 2008: Special Issue- Saluting the SCA

- Vol. 11 #18, June 26, 2008: Asia, Chapter 1

- Vol. 11 #19, July 10, 2008: Asia, Chapter 2 – The Travelogue

- Vol. 11 #2, June 4, 2007: Commencement

- Vol. 11 #20, August 29, 2008: Energy Independence

- Vol. 11 #21, September 24, 2008: Piezoelectricity

- Vol. 11 #23, December 16, 2008: Korea

- Vol. 11 #3, June 25, 2007: Alternative Energy Break-throughs

- Vol. 11 #4, July 6, 2007: Bags and Bottles

- Vol. 11 #5, July 31, 2007: Carbon and Other Carbon Issues

- Vol. 11 #7, September 12, 2007: The Big Energy Equation

- Vol. 11 #8 October 12, 2007: German Solar Research Tour 2007

- Vol. 11 #9, November 6, 2007: U.S. Energy Consumption

- Vol. 12 #1, January 7, 2009: Happy 2009

- Vol. 12 #10, August 28, 2009: Ireland Exclusive

- Vol. 12 #11, September 29, 2009: Blasting Past Net Zero

- Vol. 12 #12, October 12, 2009: California’s Water Waves

- Vol. 12 #13, November 11, 2009: Plugging In: All-Electrics and Plug-In Hybrids

- Vol. 12 #14, December 1, 2009: The Youngest Country

- Vol. 12 #2, February 6, 2009: Transformation

- Vol. 12 #3, March 9, 2009: Solar Policy

- Vol. 12 #4, March 31, 2009: Special Yosemite Edition

- Vol. 12 #5, April 26, 2009: A Collage of Good News

- Vol. 12 #6, May 8, 2009: Cross Country

- Vol. 12 #7, June 17, 2009: Special Wind Issue

- Vol. 12 #8, June 23, 2009: A Special AB 811 Conference

- Vol. 12 #9, July 24, 2009: Gardening and More

- Vol. 13 #1, January 29, 2010: EcoMotion Retreat and Mission

- Vol. 13 #10, February 23, 2011: Into the Cold

- Vol. 13 #11, March 16, 2011, Worldwide Energy Events

- Vol. 13 #12, April 5, 2011, From The Hill to My Backyard

- Vol. 13 #13, May 5, 2011: Partial Eclipse of the Moon

- Vol. 13 #14, July 20, 2011: Energy Transformation

- Vol. 13 #15, August 18, 2011: Fuel Update

- Vol. 13 #16, November 7, 2011: Ted’s Travelogue

- Vol. 13 #2, February 10, 2010: The Net Zero Carbon Study Tour

- Vol. 13 #3, March 23, 2010: Wal-Mart’s Farming

- Vol. 13 #4, March 31, 2010: The Value of Trees

- Vol. 13 #5, June 23, 2010: The Size of the Problem

- Vol. 13 #6, July 16, 2010: The Good, the Bad, and the Ugly

- Vol. 13 #7, October 1, 2010: Forging the Green Economy

- Vol. 13 #8 October 13, 2010: Stepping Up!

- Vol. 13 #9, November 19, 2010: Trekking

- Vol. 14 #1, January 31, 2012: Long Island Sound

- Vol. 14 #2, February 22, 2012: Efficiency and Economics

- Vol. 14 #3, May 9, 2012: Carbon Update

- Vol. 14 #4, May 25, 2012: Emissions Time Bomb

- Vol. 14 #5, July 3, 2012

- Vol. 14 #6, July 16, 2012

- Vol. 14 #8, Sept 2, 2012: A Pacific Northwest Eco-Travelogue

- Vol. 15 #10 June 28, 2013: Waste Management

- Vol. 15 #11 July 23, 2013: Martha’s Vineyard, Buzzards Bay and Boston

- Vol. 15 #12 August 26, 2013: The Magnificent

- Vol. 15 #6 March 22, 2013: Food trucks, Sequestration, and Zero-Emission Aviation

- Vol. 15 #7 April 8, 2013: Seared Ahi and Junior Liens

- Vol. 15 #8 May 10, 2013: 2013 New England SAVE A TON Campus Tour

- Vol. 15 #9 June 7, 2013: Wind, Solar, Efficiency, and Carbon Neutrality

- Vol. 16 #1 September 27, 2013: The Corporate Green Special

- Vol. 16 #10 March 13, 2015: The Stepchild Geothermal

- Vol. 16 #3 November 25, 2013: Visiting Pine Tree

- Vol. 16 #4 April 3, 2014: The 6,000 Year Old Solar Industry

- Vol. 16 #5 July 15, 2014: The Food Revolution

- Vol. 16 #6 September 22, 2014: Click and Mortar

- Vol. 16 #7 October 28, 2014: New England in Full Fall Glory

- Vol. 16 #8 November 26, 2014: The Best of the U.S./China Climate Deal

- Vol. 16 #9 February 12, 2015: Cool Commute

- Vol. 17 #1 July 2, 2015: The Campus Special

- Vol. 17 #2 August 26, 2015: The Dalai Lama on Climate Change

- Vol. 17 #3 September 16, 2015: Prop 39 and the Bad Rapp

- Vol. 17 #4 November 12, 2015

- Vol. 17 #5 November 19, 2015: Path to Positive

- Vol. 18 #1 March 17, 2016: Sustainability Snapshots

- Vol. 18 #2 May 25, 2017: Community Storage

- Vol. 18 #3 June 21, 2016: The Splendor of the Rockies

- Vol. 18 #4 July 20, 2016: Nuclear-Free Dreaming

- Vol. 18 #4 July 20, 2016: Nuclear-Free Dreaming

- Vol. 18 #5 August 18, 2016

- Vol. 18 #6 October 3, 2016

- Vol. 18 #7 October 29, 2017: Electricity Insurance and the Grid

- Vol. 18 #8 November 22, 2016: EcoMotion 2016 Solar Innovation Tour Special

- Vol. 19 #1 January 9, 2017: The End of Cars

- Vol. 19 #2 February 24, 2017: The “End of Drought”

- Vol. 19 #3 April 18, 2017: Essays on Senses

- Vol. 19 #4 May 23, 2017: The Dizzying Pace of Renewables

- Vol. 19 #5 July 7, 2017: Being the Light

- Vol. 19 #6 August 10, 2017: Speaking on Energy Resiliency

- Vol. 19 #6 August 30, 2017: Red Light Cameras

- Vol. 19 #8 November 2017: Honoring Milestones and Roots

- Vol. 19 #9, December 15, 2017: The PERC Project Update

- Vol. 20 #1 January 11, 2018: The EV Special

- Vol. 20 #2 March 1, 2018: New Frontiers in Sustainability

- Vol. 20 #3 April 12, 2018: Ducks and Dragons

- Vol. 20 #4: Solar Mandates and EcoMotion is in the News

- Vol. 20 #5: Floating Wind, The Little Stuff, and more

- Vol. 20 #6: Finding Jean-Luc

- Vol. 20 #7: Net Zero Energy and The Global Climate Action Summit

- Vol. 20 #8: Energy Storage in North America and CicLAvia

- Vol. 20 #9: A Special Report on the State of Recycling

- Vol. 21 #1: Recycling Action Plan and more

- Vol. 21 #3: Water, Wildfires, and Solutions

- Vol. 21 #4: Tree Planting, Styrofoam, and more

- Vol. 21 #5: Scandinavia 2019 Travelogue

- Vol. 21 #6: Offshore Wind and Solar are Booming

- Vol. 21 #7: The African Immersion

- Vol. 21 #8: Blown Away in Dubai

- Vol. 21 #9: What a Year!

- Vol. 22 #1: Big and Bold Green Steps!

- Vol. 22 #2: A Sustainable Post-Covid World

- Vol. 22 #3: Big Time Renewables

- Vol. 22 #4: Gardening, CCAs, Duck Curve, Microgrids

- Vol. 22 #5: A Green Hydrogen Future?

- Vol. 22 #6: Offshore Wind “Floaters” Poised

- Vol. 22 #7: Microgrids and Virtual Power Plants

- Vol. 23 #10: Green Car Rentals and Greenest Colleges

- Vol. 23 #11: COP26 and Carbon

- Vol. 23 #12: Taking Responsible Climate Action

- Vol. 23 #1: Net Energy Metering 3.0

- Vol. 23 #2: The End of ICE Cars

- Vol. 23 #3: Aspen Skiing Company’s Methane Capture

- Vol. 23 #4: The Earth Day / Climate Action Special

- Vol. 23 #5: Dinner with Amory

- Vol. 23 #6: The Billion Dollar Initiative

- Vol. 23 #7: EV Pickups Ready for Blast Off

- Vol. 23 #8: Fossil-Free Steel and Delivery Drones

- Vol. 23 #9: Climate Optimism and Green Cement

- Vol. 24 #10: Visiting Alaska

- Vol. 24 #11: Wind and Battery Innovations

- Vol. 24 #12: The 2022 Review; Essay on Fusion

- Vol. 24 #1: Lithium-Ion Battery Recycling

- Vol. 24 #2: Scaling Hydrogen

- Vol. 24 #3: 24/7 Carbon-Free Energy

- Vol. 24 #4: Earth Day at 52

- Vol. 24 #5: Restoration Ranch

- Vol. 24 #6: Visiting Esalen at Big Sur

- Vol. 24 #7: The Elevator Update

- Vol. 24 #8: Sailing the Coast of Maine

- Vol. 24 #9: California’s Heat Wave Heroes

- Vol.25 #10: Bloated Cars

- Vol.25 #11: The Climate Reality

- Vol.25 #12: Electric Vehicle Charging

- Vol.25 #1: Untapped Solar Potential, Sustainable Aviation, and Cigarette Butt Accountability

- Vol.25 #2: The EV Revolution

- Vol.25 #3: Oyster Bay

- Vol.25 #4: Celebrating Rocky Mountain Institute’s Impact!

- Vol.25 #5: Crafting Intentional Community

- Vol.25 #6: The Renewable Tipping Point

- Vol.25 #7: Electric Vehicle Charging Networks

- Vol.25 #8: Father of the Bride

- Vol.25 #9: The End of Range Anxiety

- Vol.26 #1: The Times They Are a’Changing

- Vol.26 #2: Solar is Surging

- Vol.26 #3: Diet, Happiness, Dancing

- Wall of Interns

- Warren Buffet Invests in Solar Farm

- Washington (VT) Electric Cooperative, Direct Install Program

- Washington State Energy Office, Energy Savings for Nonprofits

- Washington Water Power, Distribution Charge & DSM Programs

- Water Efficiency and Management

- Waverly (IA) Light and Power, Comprehensive DSM

- Western Area Power Administration, Pump Testing and Irrigation Efficiency

- Western Area Power Administration, Solar DSM

- Western Massachusetts Electric, Neighborhood Program

- Westmont Solar Energy Project by PermaCity Solar

- What Kind of Milk to Drink?

- White Paper on Community Choice Aggregation The Opportunity and its Status Nationally

- White Papers

- Who we are

- Wisconsin Electric, Appliance Turn-In Program

- Wisconsin Public Service Corporation, Wise Buys Irrigation Program