Net Energy Metering 3.0 – CALSSA

Thanks to the California Solar and Storage Association (CALSSA) for a most informative webinar on the regulatory process in California that will lead to Net Energy Metering 3.0. We salute CALSSA’s work in supporting distributed solar and storage and thank Brad Heavner for his astute perspectives and efforts.

Let’s begin with the basics: Net energy metering (NEM) allows homeowners and business owners to install solar and to send excess generation to the grid. It’s a bright sunny summer day… lots of solar. You’re generating more solar power than you can use. You send it to the grid and get credit at exactly the price you would have had to pay to buy that much power. You are getting 100% of the “retail rate.” Then in the dark and short days of winter your solar system is producing less than you use, so you draw power from the grid and expend your credits. The grid has allowed this.

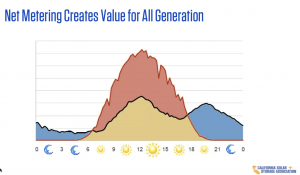

The graph above shows a typical sunny day. You can see that there’s lots of solar generation represented in red. It’s way above the yellow shaded area that represents actual site use. The solar you use onsite (the yellow area) is “behind the meter.” It’s under your control. It’s valued at the full retail rate, the price that you would have paid your utility if you did not have solar.

The area shaded red is the situation in question: That’s the amount that you “export” to the grid on those sunny days of summer. Fully 50% of all the solar kilowatt-hours generated by residential customers is “exported” to the grid through net energy metering.

Naturally, consumers want to maintain NEM as is. It’s a great deal that allows us to generate 100% of our annual usage and not at the same time as we use it. Utilities claim that this use pattern represents a subsidy paid by all ratepayers. Utilities want to pay far less for that power. In fact, it’s much more than they pay for utility-scale solar or any other generation.

As it is in other states, NEM in California is at a crossroads. It’s at a tough regulatory spot: The less value that solar owners get for the red area, the lesser the ROI, the longer the payback. Cutting the NEM value will impact the solar industry, retard job growth and economic development, and slow cities’ progress with climate action. Certainly, the economics of California’s Title 24’s solar requirement for all new homes is in jeopardy.

California has just opened a regulatory proceeding on Net Energy Metering 3.0. CALSSA’s regulatory specialist, Heavner, expects a ruling as soon as November of 2021, and implementation of the rule as early as the second quarter of 2022.

CALSSA’s policy goal and challenge are to get regulators and their utilities to continue to grow and support the solar and storage market. CALSSA and its members want the State to encourage solar interconnections through net energy metering that provides great value to solar system owners. CALSSA wants jobs, economic development, health, and resilience benefits to be factored into NEM-3.

A bit of history: California’s first NEM in 1995 was a limited program for residential customers only and for solar systems less than 10 kW in size. The program was capped at 0.1% of peak demand, or 53 MW statewide. In 2001, the program was revised to allow for systems as large as 1 MW.

Shortly thereafter, the cap was raised from 0.1% to 0.5%, boosting solar capacity allowed to 270 MW. Then SB1 in 2006, the California Million Solar Roofs raised the cap from 0.5% to 2.5%. In 2010, the cap was raised from 2.5% to 5%. In 2012, the CPUC elected to use a different calculation of peak demand which effectively doubled the cap in terms of megawatts allowed.

In 2016, NEM-2 was ordered into effect by the Commission. At the time, it made clear that this was an interim decision and NEM-3 proceedings would take place in 2019. NEM-3 would be based on deep analysis of NEM-1 and NEM-2 and would seek to resolve key issues not addressed in NEM-2.

NEM-2 has several features of note: First, it lifted the amount of solar that a company could put onsite — there’s even been a 13 MW, NEM system. NEM-2 instituted the collection of non-bypassable charges (NBCs) at a cost of 1.5 – 2 cents per kilowatt-hour of net metered solar. It also made time-of-use rates mandatory for solar customers.

NEM-2 made clear that municipal utilities were not required to go beyond the 5% cap. In fact, a number of municipal utilities have already hit the 5% mark: Merced, Imperial, Palo Alto, Alameda, and Redding. Despite CALSSA’s efforts, none are strongly advocating additional distributed solar. Anaheim Public Utilities has instituted a “Annual Cash Compensation Rate” for exported power which is essentially a wholesale rate. Even Sacramento Municipal Utility District is reportedly holding back from full support of distributed solar.

Proposals for NEM-3 are due from stakeholders in March. Stay tuned. CALSSA cautions the State not to follow the path of Hawaii and Nevada, both of which submarined their solar industries.

We do have insights now: Heavner says that many of the issues and a variety of solutions were put on the table a few years ago in the NEM-2 proceeding:

Some argued for utilities to pay solar customers an “export credit” instead of the retail rate for the area in red. (Export credit rates of 4 – 9.7 cents/kWh were proposed.) And/or, utilities could charge a fixed monthly fee or demand charges for interconnection and NEM. Another design option considered is for monthly NEM true-ups instead of annual true-ups and thereby disallowing seasonal banking of NEM credits.

The most far-out concept is that utilities could charge customers for all of their solar generation, even heretofore sacrosanct “behind-the-meter” solar. That’s the area in yellow that has always been considered “yours!” A charge of 2.4 cents was proposed.

Another intriguing option is “Buy All / Sell All,” whereby a solar customer would have two meters: one to measure how much solar energy is generated, the other measuring the site load. Naturally, utilities want to pay wholesale rates for generation while charging retail rates for consumption. Stakeholders have also looked at locational values for solar generation.

Summing it up: The biggest NEM-3 factor is the basic financial deal. Will there be an export compensation rate? Will there be fixed monthly charges for grid access? What about Buy-All, Sell All? Will specific rate requirements be tied to NEM-3? Will those that get it, get it for 20 years as has been the case for NEM-1 and NEM-2? What will the “glide path” look like from NEM-2 to NEM-3? How long will the phase in be?

Complicating matters greatly is the energy storage. Will solar + storage systems require a different tariff? One separate from solar? There are big questions about NEM-solar paired with storage. At this time, you can get NEM credit for export from storage if the storage is filled with solar electrons, and you can prove it. The more punitive the CPUC’s decision on storage, the more likely that there will be grid defection, with customers cutting the utility cord and relying solely on their own systems.

CALSSA presents the reality that in the coming years, the economics may be quite different. SGIP is slated to expire. It may get refunded, but it hasn’t yet. The ITC will step down. And if a restrictive NEM-3 hits the market. Ouch!

Examples from around the world of successful solar adoption have depended on rates even higher than retail, like Germany’s Feed-In Tariff. To retreat far short of retail values is heading in the opposite direction.